A handful of the latest CRE CLO deals lean hard into multifamily collateral and full-term interest-only structures. CRED iQ analyzed loan-level collateral across a handful of the latest CRE CLO deals totaling $4.68 billion and 160 loans of collateral, and the profile points to lenders concentrating risk in the sectors and structures they trust most in a higher-rate environment.

What property types dominate the newest CRE CLO deals?

Multifamily anchors the sample. Apartment collateral makes up 79.8% of aggregate balance in the sample, followed by hospitality at 8.1% and industrial at 5.2%. Office, retail, and healthcare each account for roughly one percent or less. The concentration confirms that CRE CLO issuers remain committed to transitional multifamily lending even as other property types stay largely on the sidelines.

Interest-only terms are nearly universal. Full-term IO loans represent 95% of collateral balance, with the small remainder carrying partial IO or amortization. The structure preserves borrower cash flow during business-plan execution, but it also means principal paydown is minimal until maturity, keeping refinancing pressure front and center. The sampled pools carry a weighted-average spread of 303 basis points over SOFR and a weighted-average coupon near 6.68%.

What does this signal for CRE CLO issuance in 2026?

These deals point to a familiar core: multifamily assets, floating-rate coupons, and IO structures that maximize early cash flow. Future funding commitments total $244 million across these deals, signaling continued appetite to finance value-add and lease-up business plans. Geographic exposure skews toward New York, Florida, and Texas, which together account for more than 43% of balance.

For investors, the takeaway is concentration. These deals offer exposure to a tightly defined slice of the market, and the reliance on full-term IO means credit performance will hinge on borrowers refinancing or selling at maturity rather than deleveraging along the way.

Source: CRED iQ proprietary analytics. Figures reflect loan-level collateral across a sample of recent CRE CLO transactions. Descriptive, not a forecast.

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market — spanning CMBS, SASB, CRE CLO, and GSE/Agency Multifamily. Delivered via web platform, API, bulk feeds, and MCP server, CRED iQ is the data provider of choice for institutional market participants and the canonical data layer for AI-driven CRE workflows. Learn more at www.cred-iq.com.

A data briefing on the composition of $6.1 trillion in U.S. bank real estate loans

By the CRED iQ Research Team · Bank Loan Analytics

Summary. U.S. bank real estate loan balances totaled $6.14 trillion in the first quarter of 2026. Since the first quarter of 2019, the composition of that book has shifted measurably. Multifamily balances grew the fastest in percentage terms, rising about 53%, while the much larger residential book grew about 17%. In dollar terms the ordering differs: core CRE and residential each added more than $440 billion, and multifamily added about $229 billion. This briefing presents the underlying figures and the methodology behind them, without forecast or recommendation.

The data

The figures below draw on CRED iQ bank loan analytics and cover all FDIC-insured commercial, savings, and community banks. Balances are outstanding loan amounts as of quarter-end. Indexing each category to its first-quarter 2019 level (set to 100) isolates growth from the large differences in starting size across property types.

As of the first quarter of 2026, multifamily balances stood at an index of 153 (about 53% above the 2019 level), core CRE at 132 (about 32%), construction and development at 128 (about 28%), and residential at 117 (about 17%). Residential, which comprises 1-4 family residential mortgages and home equity, remained the largest category at $3.10 trillion, roughly half of all bank real estate lending, followed by core CRE at $1.92 trillion, multifamily at $665 billion, and construction at $453 billion.

Percentage growth and dollar growth diverge

Growth measured in percent and growth measured in dollars point to different segments. Residential added approximately $445 billion in outstanding balances since the first quarter of 2019 and core CRE added approximately $467 billion, each exceeding the roughly $229 billion added by multifamily, despite multifamily posting the largest percentage gain. The distinction matters for gauging where the largest absolute exposures have accumulated on bank balance sheets, as opposed to where growth has been proportionally most rapid.

Construction and development: a distinct pattern

Among the four categories, construction and development shows the most pronounced change in direction. Indexed to 2019, construction balances rose to a peak near 142 in 2024 before declining into early 2026, ending at 128. This rise-and-partial-reversal pattern is consistent with a period of expanded development lending that has since moderated. It is specific to the post-2019 window and is not evident in longer time series that are shaped by the sector’s post-2008 contraction and recovery.

Balances reflect outstanding loans held by FDIC-insured institutions and exclude loans originated and sold into secondary markets. A substantial share of newly originated 1-4 family mortgages is securitized rather than retained on bank balance sheets, which is one factor behind residential’s comparatively modest balance-sheet growth relative to origination activity. Property-type categories follow standard bank regulatory classifications: nonfarm nonresidential (core CRE), multifamily residential, construction and development, and 1-4 family residential plus home equity (residential). Index values are computed as the ratio of each quarter’s balance to the first-quarter 2019 balance, multiplied by 100.

Source: CRED iQ Bank Loan Analytics and Bank Data Analysis, as of Q1 2026. Balances indexed to Q1 2019 = 100. Figures reflect all FDIC-insured commercial, savings, and community banks. This briefing is descriptive and does not constitute a forecast or investment advice.

Data scientist and CRE technology leader to drive the company’s next generation of AI-powered data products

PHILADELPHIA, PA — CRED iQ, a leading commercial real estate data and analytics platform, today announced the appointment of Liam Mulcahy as Senior Product Manager, CRE Data & Applied AI. In the role, Mulcahy will lead the development of new data and analytics products that pair CRED iQ’s proprietary distress and loan-level intelligence with applied artificial intelligence.

Mulcahy brings a rare combination of data engineering, applied AI, and commercial real estate experience to CRED iQ. He most recently co-founded an AI analytics venture focused on helping commercial real estate firms compete in AI search, where he built multi-model data pipelines spanning the major large language model platforms and a broker-facing analytics dashboard. Earlier, he led revenue and pricing strategy across a 3,500-plus unit multifamily portfolio at Post Brothers, and spent several years at CoStar Group building data automation, business intelligence, and machine learning tools while working directly with brokers, owners, and investors. He holds a Master of Science in Data Science from the University of Virginia.

“The CRE market is moving faster than the tools most firms use to read it, and we don’t close that gap by hiring product managers, we hire people who’ve lived the problem,” said Michael Haas, Founder and CEO of CRED iQ. “Liam has built data systems at CoStar, run revenue for a 3,500-unit portfolio, and shipped AI analytics for CRE. He joins us to pair that experience with our proprietary distress and loan-level data so our clients see risk and opportunity before anyone else does.”

In his new role, Mulcahy will own data and analytics products end to end, partnering across engineering, sales, and customer success. His early focus will include smarter trigger-event detection and new AI-driven ways for CRED iQ customers to work with the company’s data.

“CRED iQ has built something the market genuinely relies on, and the data underneath it is exceptional, and customers want to bring this data into their AI workflows.” said Mulcahy. “The opportunity to apply AI to that foundation, and to build tools that help our customers act faster and with more confidence, is exactly the work I want to be doing. I’m thrilled to join the team.”

About CRED iQ

CRED iQ is a commercial real estate data and analytics platform serving CMBS analysts, special servicers, lenders, brokers, and investors. The company’s proprietary distress and loan-level data gives clients a differentiated, real-time view of the market, powering research, underwriting, and origination workflows. CRED iQ is headquartered in Philadelphia, Pennsylvania.

CRED iQ Research | Q1 2026 | Multifamily Bank Loan Performance

The overall multifamily delinquency rate at FDIC-insured banks climbed to 1.47% in Q1 2026, up 5 basis points from 1.42% at year-end 2025, according to CRED iQ analysis of the latest Banking data. Delinquent multifamily balances reached $9.78 billion, the largest dollar amount since Q1 2011, even as bank multifamily portfolios continued to expand to a record $665.3 billion.

What Do Banks’ Q1 2026 Numbers Show for Multifamily?

CRED iQ tracks bank multifamily performance across three measures. Loans 30-89 days past due rose to 0.40% of balances, or $2.66 billion, up from 0.38% in Q4 2025. Loans 90+ days past due or in nonaccrual status, the seriously delinquent bucket, rose 3 basis points to 1.07%, with dollar volume increasing to $7.12 billion from $6.86 billion. Combined, the overall delinquency rate of 1.47% matches the Q1 2025 reading and marks the joint-highest level of this cycle. The Banking Report itself flagged multifamily past-due and nonaccrual rates as remaining elevated in its Q1 2026 release.

How Does 1.47% Compare Historically?

Outside of the matching Q1 2025 print, banks have not reported multifamily delinquency this high since Q2 2013, when the industry was still working down Global Financial Crisis credit. Today’s rate remains far below the GFC peak of 5.90% set in Q1 2010, when $12.68 billion was delinquent against a much smaller loan base. The more telling comparison is the cycle low: multifamily delinquency bottomed at just 0.21% in Q3 2019, meaning the current rate is seven times its pre-pandemic trough.

Are Banks Still Growing Their Multifamily Books?

Yes. Multifamily loans outstanding at FDIC-insured institutions rose 0.9% quarter over quarter and 4.1% year over year to $665.3 billion, roughly 3.5 times the $192 billion held in early 2007. Growing denominators have masked some of the dollar deterioration: delinquent balances are up $415 million in a single quarter and now sit at 15-year highs even while the rate itself appears moderate.

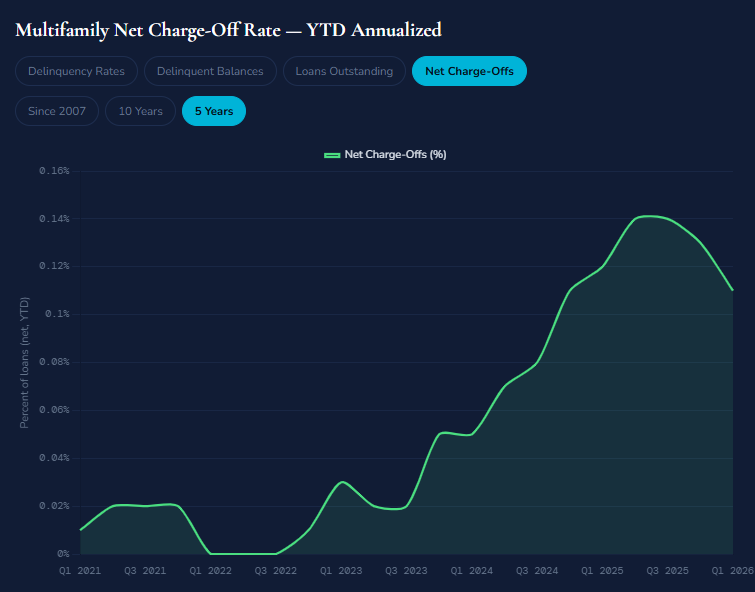

What Are Losses Telling Us?

Realized pain remains limited. The multifamily net charge-off rate ran at just 0.11% annualized in Q1 2026, down from 0.13% for full-year 2025. The gap between rising delinquency and muted charge-offs suggests banks are still resolving troubled multifamily credit through extensions and workouts rather than write-downs, a dynamic CRED iQ also observes across CMBS loan modifications.

The Bottom Line

Bank multifamily credit is deteriorating gradually, not collapsing. With $9.78 billion delinquent and balance growth still outpacing resolutions, Q2 2026 data will show whether the seasonal Q1 bump fades or compounds. Explore the full interactive tracker and request the underlying data at cred-iq.com.

Source: CRED iQ analysis of all FDIC-insured institutions, multifamily residential real estate loans, Q1 2007 through Q1 2026.

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market — spanning CMBS, SASB, CRE CLO, and GSE/Agency Multifamily. Delivered via web platform, API, bulk feeds, and MCP server, CRED iQ is the data provider of choice for institutional market participants and the canonical data layer for AI-driven CRE workflows. Learn more at www.cred-iq.com.

CRED iQ Research | Proprietary Multifamily & CMBS Loan Analytics

Across eight Freddie Mac multifamily securitizations priced in early 2026, underwriting has tightened decisively: weighted-average debt service coverage on the conduit K-series sits at 1.41x against a 63.9% loan-to-value, with full-term or partial interest-only structures attached to roughly 95% of balance.

CRED iQ analyzed the loan-level annexes behind FREMF 2026-K179, K180, K561, K562, K563, K766, the floating-rate KF172, and the small-balance Q040, representing 472 loans and more than $7.2 billion in unpaid principal. The picture that emerges is a market that has repriced risk without abandoning leverage, leaning on interest-only relief to keep coverage above water while the rate curve stays elevated. Below we walk the dominant underwriting themes, the originators driving the volume, three loans that bring those themes to life, and where the second half of 2026 is likely headed.

What are the dominant underwriting themes in the 2026 Freddie K-series?

Coverage is being manufactured through structure, not cash flow. Fixed-rate K-deals cleared with weighted DSCRs between 1.35x and 1.51x, but those figures lean heavily on interest-only periods. Full-term IO carried about 30% of K-series balance and partial IO another 65%, meaning amortizing dollars are now the exception rather than the rule. Strip the IO benefit away and several loans underwrite near or below 1.20x on a fully amortizing basis.

Leverage held, pricing did the adjusting. Weighted LTVs clustered in the low-to-mid 60s across the fixed-rate book, in line with historical Freddie discipline. What moved was coupon: gross rates ranged from roughly 4.9% on the cleanest refinances to 5.66% on the floating KF172 pool. Acquisition activity made up about 40% of K-series balance, a healthy sign that transaction volume is returning even as borrowers absorb higher carry.

The floating-rate pool is where the stress concentrates. KF172 underwrote to a 1.21x weighted DSCR and a 68.7% LTV, the thinnest and most levered of the group, with every loan carrying SOFR-based pricing and mandatory rate caps. This is the segment to watch: coverage that looks adequate on an IO basis compresses fast if SOFR stays sticky into refinancing windows.

Who are the top originators in the 2026 K-series?

Origination is concentrated among a handful of agency specialists. CBRE Capital Markets leads with roughly $1.42 billion across the eight deals, about 20% of pooled balance, followed by Berkadia at $1.05 billion and Walker & Dunlop at $680 million. Those three alone account for more than 43% of issuance. JPMorgan Chase ranks fourth by balance but first by loan count, driven by its 228 small-balance loans in the Q040 pool. JLL, PNC Bank, Capital One, Lument, KeyBank, and PGIM round out the top ten.

The credit signal is in the spread between shops. PNC Bank’s book carries the strongest weighted coverage among large originators at 1.61x, while Lument’s sits at 1.29x, reflecting a more leveraged, IO-heavy mix. CBRE and Berkadia, the two largest, underwrite near the pool average at 1.43x and 1.35x respectively. The takeaway: balance leadership and credit conservatism are not the same thing, and the originators pushing the most paper are not always the ones pushing the thinnest coverage.

Which loans best illustrate how 2026 deals are being underwritten?

Three loans capture the spread of risk appetite in these pools, from conservative refinance to leveraged value-add acquisition.

Centerpointe II (K179)

Rodgers Forge (K180)

Canterbury Green (KF172)

Irvine, CA — refinance

Baltimore, MD — acquisition

Fort Wayne, IN — acquisition

$140.1M balance

$78.9M balance

$159.9M balance

1.48x DSCR / 64.9% LTV

1.28x DSCR / 73.4% LTV

1.17x DSCR / 74.1% LTV

Full-term IO, 5.11% fixed

Partial IO, 5.20% fixed

Floating, 30-day SOFR + 1.87%

Built 2015, 372 units

Built 1945, 498 units

Built 1970, 2,000 units

Centerpointe II is the template for a clean 2026 refinance. A 2015-vintage Irvine asset at 95.4% occupancy, it carries a full-term interest-only loan at a 1.48x DSCR and a conservative 64.9% LTV against a $216 million appraisal. The borrower is not stretching; the IO simply preserves cash flow at a 5.11% coupon. This is the kind of credit Freddie can underwrite all day.

Rodgers Forge shows the cost of acquiring older product. The 1945-built, 498-unit Baltimore property was renovated in 2010 and trades at a 73.4% LTV with a partial-IO structure that lifts coverage to 1.60x during the IO window but settles to 1.28x once amortization begins. At a $158,000 balance per unit it is reasonably priced, yet the amortizing coverage leaves little room if expenses on a 1940s asset surprise to the upside.

Canterbury Green is the pool’s pressure point. At $159.9 million it is the single largest loan across all seven deals, a 2,000-unit Fort Wayne acquisition underwritten to just 1.17x amortizing coverage and a 74.1% LTV on floating-rate debt indexed to 30-day SOFR. The interest-only DSCR of 1.42x masks how thin the amortizing math is. A rate cap is required, but cap protection expires, and refinancing 2,000 units of 1970s garden product into a higher-for-longer curve is precisely the scenario that keeps credit officers up at night.

What does this mean for the second half of 2026?

We expect interest-only reliance to peak and then retreat. Lenders cannot keep pushing coverage uphill on IO alone; as the curve normalizes, look for amortizing structures to creep back into K-deals and for full-term IO to fall below a quarter of balance by year-end.

The floating-rate book will define the next distress cycle, if there is one. CRED iQ’s view is that fixed-rate K-series credit is sound, but pools like KF172 concentrate the refinancing and cap-expiry risk. Watch the sub-1.25x amortizing coverage loans in Florida and the Midwest garden segment; that is where any 2026 deterioration shows up first.

Acquisition volume keeps building. With acquisitions already near 40% of K-series balance and refinances pricing cleanly in the high-4% to low-5% range, transaction activity should accelerate into the back half of the year. Our bold call: by Q4 2026, acquisition share of new K-series issuance crosses 50% for the first time since the rate shock, signaling that multifamily price discovery has finally caught up to the cost of capital.

The bottom line: Freddie’s 2026 underwriting is disciplined on leverage, aggressive on structure, and quietly concentrating its real risk in the floating-rate corner of the program. The fixed-rate book should perform. The floating-rate book is the one to model loan by loan.

Data attributed to CRED iQ proprietary loan analytics. Figures are balance-weighted across loan-level annex disclosures for FREMF 2026-K179, K180, K561, K562, K563, K766, KF172, and Q040. cred-iq.com

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market — spanning CMBS, SASB, CRE CLO, and GSE/Agency Multifamily. Delivered via web platform, API, bulk feeds, and MCP server, CRED iQ is the data provider of choice for institutional market participants and the canonical data layer for AI-driven CRE workflows. Learn more at www.cred-iq.com.

CRED iQ’s overall CMBS distress rate rose to 11.86% in May 2026, up from 11.08% in April, as both special servicing and delinquency moved higher across the Conduit and SASB universe. The reversal erased April’s brief improvement and pushed distress back toward the cyclical highs observed across the trailing twelve months. Viewed over a longer horizon, the trajectory is unmistakable: the overall distress rate has more than doubled since mid-2022, when it sat near 5%, underscoring that resolution activity is not yet keeping pace with new transfers into distress.

What is the CRED iQ distress rate?

CRED iQ defines its overall distress rate as the balance-weighted share of loans that are either delinquent, in special servicing, or both. This combined lens captures stress that headline delinquency figures alone can miss, because a loan can transfer to a special servicer for imminent default, maturity default, or covenant breaches well before it misses a payment. Measured across the full Conduit and SASB universe, the May 2026 reading reflects a broad, balance-weighted view of credit performance rather than a simple loan count.

How did the three distress metrics move in May 2026?

All three core measures CRED iQ tracks turned higher month-over-month:

Overall distress rate: 11.86%, up 78 basis points from 11.08% in April.

Special servicing rate: 11.25%, up 64 basis points from 10.61%.

Delinquency rate: 9.53%, up 58 basis points from 8.95%.

The persistent gap between the special servicing rate and the delinquency rate — roughly 170 basis points in May — signals that a meaningful share of distressed balance is being actively worked out by servicers before, or instead of, becoming payment-delinquent. For investors and lenders, that spread is a leading indicator worth monitoring as 2026 and 2027 maturities approach.

Which property types are driving CMBS distress?

Office remains the clear epicenter of distress at a 17.11% distress rate — the most troubled major segment. Mixed-use follows at 16.12%, while lodging (12.27%) sits above the overall average. Multifamily distress reached 10.95% as elevated rates continue to pressure floating-rate and bridge financing. At the opposite end, the resilience leaders are striking: self storage (0.15%), industrial (1.04%), and manufactured housing (1.19%) all remain near-pristine, reflecting durable demand fundamentals and stable, granular cash flows.

Property Type

Distress

Special Servicing

Delinquency

Office

17.11%

16.83%

13.91%

Mixed Use

16.12%

14.41%

14.23%

Lodging

12.27%

10.18%

9.49%

Multifamily

10.95%

10.36%

8.67%

Retail

9.97%

9.75%

7.32%

Warehouse

1.83%

1.83%

1.62%

Manufactured Housing

1.19%

0.00%

1.19%

Industrial

1.04%

0.98%

0.95%

Self Storage

0.15%

0.15%

0.15%

Balance-weighted rates, Conduit + SASB, May 2026 reporting period. Source: CRED iQ proprietary loan analytics.

Why CRED iQ data matters

CRED iQ’s analytics program is built on granular, loan-level data spanning the full Conduit, SASB, Freddie Mac, and CRE CLO universe, refreshed every reporting period and resolvable down to individual loans, properties, and metropolitan markets. Because every metric is balance-weighted and traceable to the underlying collateral, market participants can move beyond headline averages to underwrite distress by property type, vintage, servicer, and geography. For CRE and CMBS investors, brokers, and lenders, that level of transparency turns distress monitoring into an actionable edge — identifying troubled credits, surfacing workout opportunities, and benchmarking portfolios against the broader market in real time.

Source: CRED iQ proprietary loan analytics | Reporting period: May 2026 | cred-iq.com

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market — spanning CMBS, SASB, CRE CLO, and GSE/Agency Multifamily. Delivered via web platform, API, bulk feeds, and MCP server, CRED iQ is the data provider of choice for institutional market participants and the canonical data layer for AI-driven CRE workflows. Learn more at www.cred-iq.com.

CRED iQ analyzed $26.1 billion of the most recently issued loans securitized in 2026 across CMBS conduit, single-asset/single-borrower (SASB), Freddie Mac, and CRE CLO transactions — and the data exposes a market split cleanly in two. On a balance-weighted basis, the average cap rate on newly originated collateral now sits almost exactly on top of the average mortgage coupon, meaning the typical 2026 borrower is financing at roughly zero positive leverage. Where a property sits relative to that line depends almost entirely on property type.

What Are Cap Rates on New CMBS Loans in 2026?

Cap rates on 2026 new-issue collateral range from 5.41% to 8.02% by property type, according to CRED iQ’s proprietary loan analytics. The balance-weighted rankings:

Hospitality — 8.02% (coupon 6.78%)

Office — 7.45% (coupon 6.50%)

Retail — 6.81% (coupon 6.61%)

Mixed Use — 6.10% (coupon 6.53%)

Industrial — 6.03% (coupon 6.33%)

Self Storage — 5.70% (coupon 6.05%)

Multifamily — 5.45% (coupon 5.64%)

Manufactured Housing — 5.41% (coupon 6.27%)

Within subtypes, the dispersion widens further. Super-regional malls priced at an 8.94% weighted cap rate — nearly 250 basis points above anchored retail centers at 6.48% — while garden multifamily (5.51%) and multifamily cooperatives (4.89%) anchored the low end.

Which Property Types Are Financing at Negative Leverage?

Every “favored” income sector is now borrowing through its cap rate. Manufactured housing (−86 bps), mixed use (−43 bps), self storage (−35 bps), industrial (−30 bps), and multifamily (−19 bps) all carry coupons above their going-in yields. Sponsors are explicitly underwriting NOI growth — or betting on lower refinancing rates — to make the math work. In contrast, hospitality (+124 bps), office (+95 bps), and retail (+20 bps) are the only sectors still delivering positive leverage, compensation for the credit risk lenders perceive there.

How Conservative Is 2026 Office and Hotel Underwriting?

Extremely. Office loans that cleared the securitization market in 2026 carry a 13.8% weighted NCF debt yield and just 55.4% cut-off LTV — the most conservative credit profile of any major sector. Hospitality runs nearly identical at a 13.8% debt yield. Only well-leased, low-leverage office is getting financed; everything else remains shut out. Multifamily, by comparison, prices at a 9.6% debt yield and 62.9% LTV, with Freddie Mac executions averaging a 4.98% coupon — roughly 145 basis points inside conduit multifamily at 6.44%, a powerful agency funding advantage.

What Does Zero Positive Leverage Mean for CRE Investors?

Three takeaways from CRED iQ’s 2026 new-issue data stand out. First, 56% of new-issue balance is full-term interest-only — borrowers are maximizing cash flow to offset thin leverage spreads. Second, the cap-rate floor has been set by debt costs, not buyer optimism: until coupons fall, multifamily and industrial cap rates have little room to compress. Third, the wide positive leverage in hotels, office, and malls signals where repricing is complete — and where opportunistic credit is being paid to take risk.

All figures are balance-weighted and sourced from the CRED iQ Proprietary Loan Analytics Platform.

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market — spanning CMBS, SASB, CRE CLO, and GSE/Agency Multifamily. Delivered via web platform, API, bulk feeds, and MCP server, CRED iQ is the data provider of choice for institutional market participants and the canonical data layer for AI-driven CRE workflows. Learn more at www.cred-iq.com.

CRED iQ’s May 2026 CMBS distress analysis reveals widening stress across the nation’s largest metropolitan markets — with the overall distress rate among the top 25 most populous U.S. MSAs climbing to 12.7%, up from 12.2% in June 2025. Seventeen of the 25 markets posted year-over-year increases, led by explosive moves in Midwest and mid-major markets.

Which U.S. Markets Have the Highest CMBS Distress Rates in 2026?

Minneapolis (55.2%), Denver (43.0%), and Rochester (40.1%) lead the top 25 largest markets in overall CMBS distress as of May 2026, according to CRED iQ’s proprietary loan analytics platform covering Conduit and SBLL pools. These figures capture all loans classified as delinquent, in special servicing, or in REO status — giving the most complete picture of loan-level stress available in the market. Minneapolis and Denver’s elevated readings reflect deep office loan impairment in their central business districts, with several large SBLL loans remaining in extended special servicing. Rochester’s distress is concentrated in a narrow but deeply stressed loan pool, amplifying its percentage reading.

At the other end of the spectrum, New York (12.0%), San Antonio (14.7%), and Houston (14.7%) post the lowest distress readings among the top 25 — a reflection of deeper, more diversified loan pools that absorb individual loan failures without dramatically moving the overall rate.

Where Is CMBS Distress Rising Fastest Year-Over-Year?

The most dramatic year-over-year escalation belongs to St. Louis (+29.9 percentage points), Oklahoma City (+28.5pp), and Pittsburgh (+16.0pp) — markets where concentrated office and mixed-use loan exposure has rapidly deteriorated. St. Louis’s distress rate climbed from just 8.2% in June 2025 to 38.1% in May 2026, the largest single-year surge in the cohort and a clear signal of accelerating loan impairment in a market facing structural office demand headwinds. Oklahoma City similarly jumped from 11.5% to 40.0%, driven by a wave of newly transferred special servicing designations.

Denver (+15.8pp) and Louisville (+15.4pp) also logged significant deterioration, reinforcing a broader pattern: mid-major metros with high legacy office concentrations and maturing floating-rate debt vintage 2021–2022 are experiencing the sharpest stress acceleration.

Which Markets Are Improving — and Why?

Not all movement is negative. Providence, RI posted the sharpest improvement in the cohort, falling 14.7 percentage points to 15.2% as previously troubled loans resolved through modification, payoff, or disposition. Charlotte, NC (-9.9pp) and Austin, TX (-9.4pp) also improved materially, consistent with stronger Sun Belt absorption dynamics and active loan workout activity in those markets. These declines highlight an important nuance in CMBS distress analysis: improvement in the rate does not always mean underlying credit quality has recovered — it can reflect successful loan resolutions at a discount rather than stabilized property performance.

Office distress nationally across these 25 markets stands at 17.1% — nearly unchanged from 17.2% in June 2025 — while Multifamily continues to creep higher, reaching 11.0% versus 10.3% a year prior. CRED iQ will continue tracking loan-level modification trends, maturity extensions, and special servicing resolution rates across all markets. Full underlying loan data is available through the CRED iQ platform.

Source: CRED iQ Proprietary CMBS Loan Analytics | Conduit & SBLL | May 2026 | cred-iq.com

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market. By aggregating, normalizing, and enriching loan-level data across the full universe of CMBS Conduit, SASB, CRE CLO, and GSE/Agency Multifamily (Freddie Mac, Fannie Mae, Ginnie Mae, and FHA/HUD), CRED iQ delivers unprecedented transparency into property performance, loan structures, and borrower exposure — bringing efficiency and analytical depth to the entire asset class. Through its web platform, API, bulk data feeds, MCP server, and CRED AI professional services division, market participants and AI systems access the industry’s most comprehensive and reliable source of deal intelligence. As the canonical data layer for AI-driven CRE workflows, CRED iQ is the data provider of choice for institutional lenders, investors, servicers, and advisors — and the foundational infrastructure for the next generation of AI applications built on top of the multi-trillion-dollar securitized CRE market. For more information, visit www.cred-iq.com.

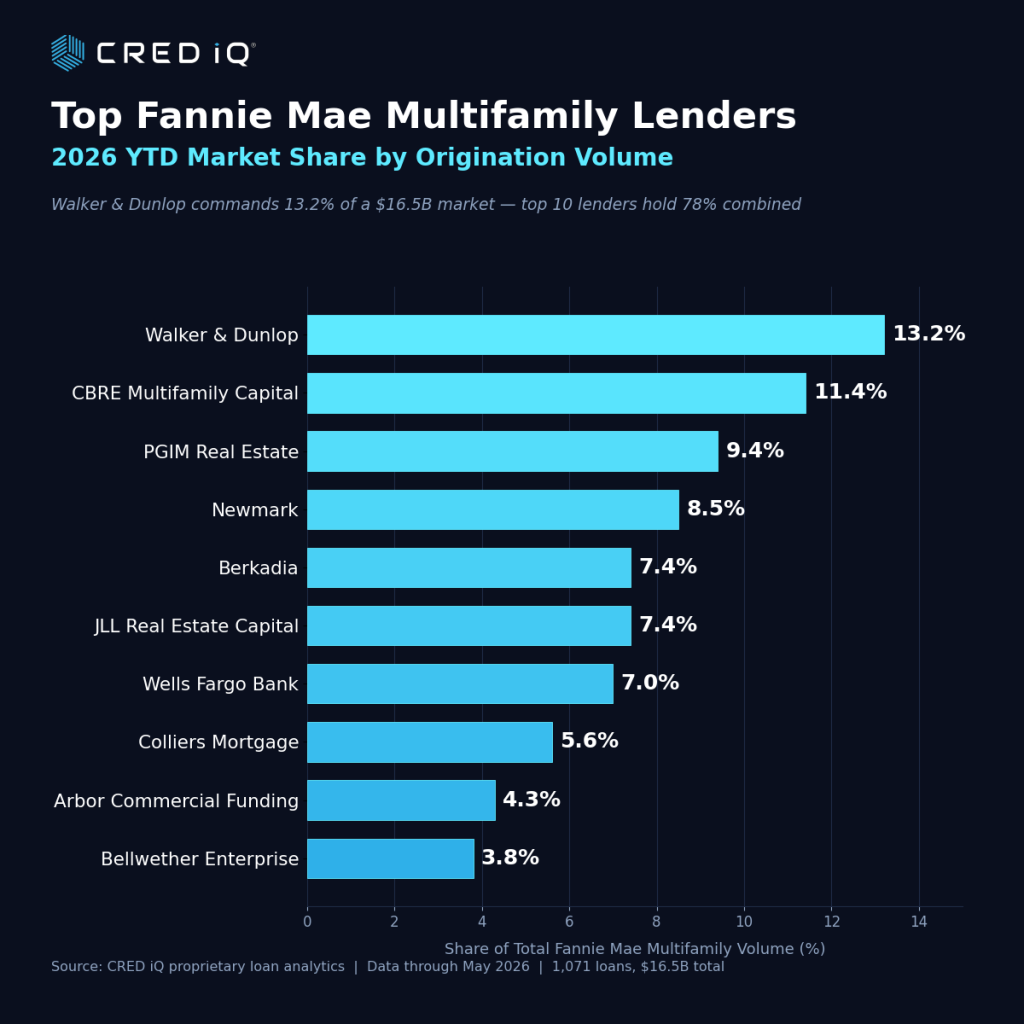

Walker & Dunlop is the top Fannie Mae multifamily lender in 2026 year-to-date, originating $2.18 billion across 110 loans, according to CRED iQ proprietary loan analytics. The firm leads a concentrated agency lending market in which the ten largest originators captured roughly 78% of all volume through mid-May.

CRED iQ analyzed 1,071 Fannie Mae multifamily loans totaling $16.5 billion issued from January through May 2026. The data reveals a market dominated by a familiar set of agency lending heavyweights, with the top five originators alone responsible for half of all dollar volume.

Who Are the Top Fannie Mae Multifamily Lenders in 2026?

The leaderboard reflects the entrenched scale advantages of the largest DUS lenders. Walker & Dunlop’s $2.18 billion narrowly outpaced CBRE Multifamily Capital at $1.88 billion and PGIM Real Estate Agency Financing at $1.56 billion. Newmark ($1.39 billion), JLL Real Estate Capital ($1.22 billion), and Berkadia ($1.22 billion) rounded out the upper tier.

The ten largest Fannie Mae multifamily originators in 2026 YTD, ranked by loan volume, are:

Loan count tells a complementary story about origination strategy. Berkadia led all lenders with 172 loans, signaling a high-volume, smaller-balance footprint, while Walker & Dunlop’s 110 loans carried a higher average balance. The average Fannie Mae multifamily loan in 2026 YTD measured approximately $15.4 million.

Is Fannie Mae Multifamily Lending Growing in 2026?

Fannie Mae multifamily origination volume accelerated through the first quarter of 2026 before moderating. Monthly volume climbed from roughly $3.1 billion in January to a 2026 peak of $5.6 billion in March, according to CRED iQ data, as borrowers moved to lock financing amid shifting rate expectations. March alone accounted for more than one-third of first-quarter volume.

What Is Driving Fannie Mae Multifamily Loan Demand?

Refinancing is the primary engine of 2026 agency activity. Refinance loans represented 62.8% of total volume ($10.3 billion), reflecting a wave of borrowers addressing 2026 and 2027 loan maturities and replacing higher-cost bridge debt. Acquisition financing accounted for 36.1% ($5.95 billion), with supplemental loans making up the small remainder. The refinance-heavy mix underscores how maturity management—rather than transaction velocity—is defining this lending cycle.

Which Markets Are Attracting the Most Fannie Mae Capital?

Gateway and Sun Belt metros dominated 2026 deployment. The New York–Newark–Jersey City MSA led all markets with $1.6 billion in Fannie Mae multifamily volume, followed by San Jose–Sunnyvale–Santa Clara ($0.75 billion) and Los Angeles–Long Beach–Anaheim ($0.72 billion). High-growth Sun Belt markets including Phoenix ($0.69 billion), Miami–Fort Lauderdale ($0.63 billion), and Dallas–Fort Worth ($0.60 billion) also ranked among the top destinations for agency capital.

The Bottom Line for CRE Lenders and Investors

The 2026 Fannie Mae multifamily landscape is defined by concentration, refinancing demand, and resilient gateway-market appetite. With the top ten lenders controlling nearly four-fifths of volume, scale and DUS relationships remain decisive competitive advantages. For investors and lenders monitoring agency capital flows, CRED iQ proprietary loan analytics offers loan-level visibility into originator activity, market deployment, and emerging refinancing trends shaping the multifamily debt cycle.

Source: CRED iQ proprietary loan analytics. Data reflects Fannie Mae multifamily loans originated January 1–May 13, 2026.

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market. By aggregating, normalizing, and enriching loan-level data across the full universe of CMBS Conduit, SASB, CRE CLO, and GSE/Agency Multifamily (Freddie Mac, Fannie Mae, Ginnie Mae, and FHA/HUD), CRED iQ delivers unprecedented transparency into property performance, loan structures, and borrower exposure — bringing efficiency and analytical depth to the entire asset class. Through its web platform, API, bulk data feeds, MCP server, and CRED AI professional services division, market participants and AI systems access the industry’s most comprehensive and reliable source of deal intelligence. As the canonical data layer for AI-driven CRE workflows, CRED iQ is the data provider of choice for institutional lenders, investors, servicers, and advisors — and the foundational infrastructure for the next generation of AI applications built on top of the multi-trillion-dollar securitized CRE market. For more information, visit www.cred-iq.com.

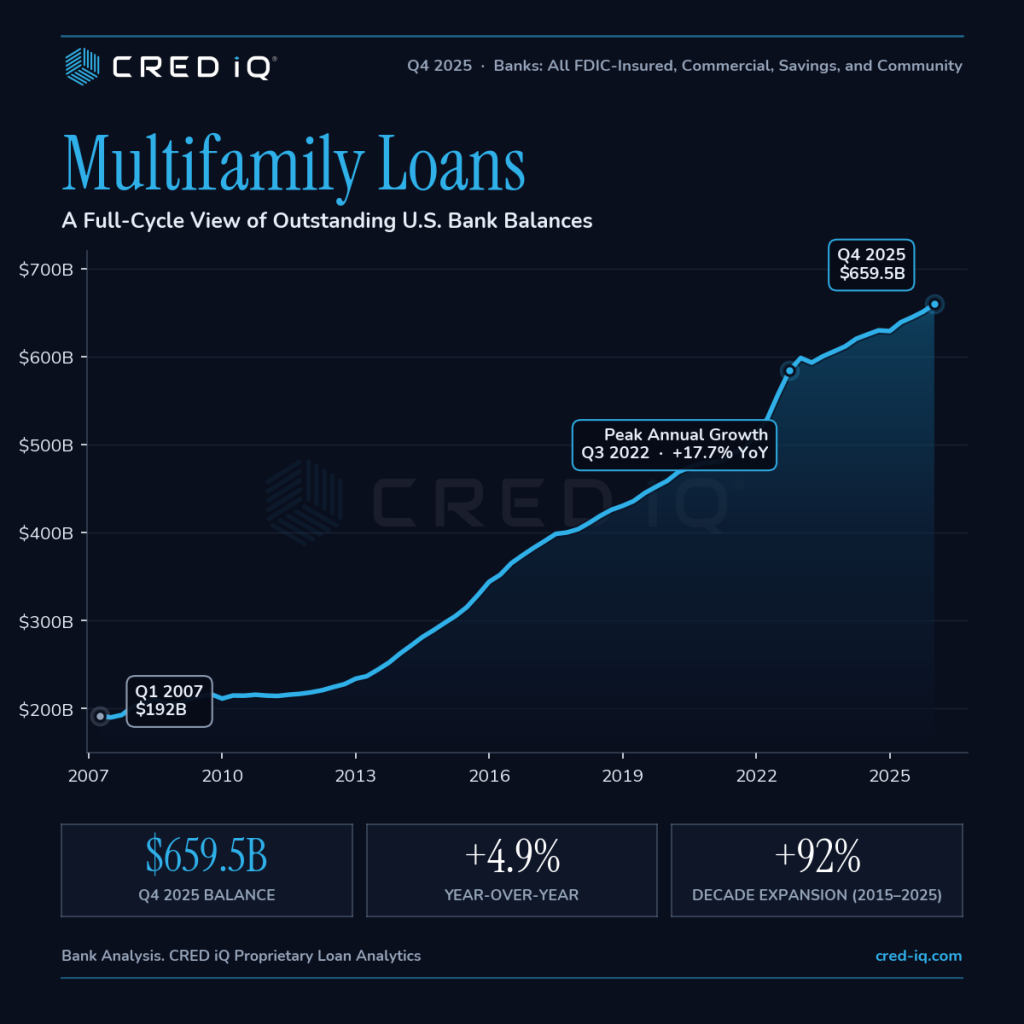

Multifamily loan balances at U.S. banks rose to a record $659.5 billion in Q4 2025, up 4.9% year-over-year, even as the multifamily delinquency rate climbed to 1.42% — the highest level since Q2 2013, according to CRED iQ’s proprietary loan analytics. The divergence between continued portfolio growth and accelerating credit stress marks one of the most consequential cross-currents in U.S. bank commercial real estate lending heading into 2026.

How Large Is the U.S. Bank Multifamily Loan Portfolio?

Outstanding multifamily loan balances at U.S. banks have grown 92% over the past decade, expanding from $344.1 billion in Q4 2015 to $659.5 billion in Q4 2025. The portfolio reached an all-time high in the fourth quarter, with quarter-over-quarter growth of $8.6 billion. Unlike construction and development lending, which has contracted for six consecutive quarters, bank multifamily exposure continues to expand — albeit at a moderating pace from the +17.7% year-over-year peak recorded in Q3 2022.

Why Are Multifamily Delinquencies Rising So Quickly?

CRED iQ’s analysis points to a confluence of pressures: elevated debt service costs at refinancing, weaker rent growth across pandemic-era boom markets (particularly Sun Belt metros that saw heavy supply deliveries), and tighter underwriting standards constraining take-out financing. The multifamily delinquency rate has risen from a cycle low of 0.24% in Q3 2022 to 1.42% in Q4 2025 — a nearly six-fold increase in just over three years.

Which Loans Are Driving the Stress?

The deterioration is concentrated in more severe delinquency stages. The 90+ day past-due / nonaccrual rate stands at 1.04% in Q4 2025, up from just 0.15% in Q3 2022. By contrast, the 30–89 day past-due rate remains comparatively contained at 0.38%, suggesting that the bulk of currently stressed loans have already migrated into deeper delinquency rather than new early-stage problems entering the pipeline at an accelerating rate.

How Does Current Stress Compare to the Global Financial Crisis?

The current 1.42% multifamily delinquency rate is materially elevated by post-pandemic standards but remains well below GFC-era stress. Bank multifamily delinquencies peaked at 5.90% in Q1 2010, with the 90+ day rate alone reaching 4.62%. Today’s readings represent roughly 24% of that GFC peak. Annualized loss rates on multifamily loans also remain modest at 0.13% in Q4 2025, compared with peak losses of 1.24% in Q4 2010.

What Does Rising Multifamily Stress Mean for Lenders and Investors?

For lenders, the divergence between portfolio growth and credit deterioration creates a complicated risk-management picture: balance sheet exposure is still expanding while the quality of existing exposure weakens. For investors and operators, distressed multifamily opportunities are likely to grow through 2026 as 90+ day delinquencies work through workout and disposition channels. The trajectory of further stress will depend largely on the path of interest rates, rent growth in oversupplied markets, and the willingness of lenders to extend modifications on maturing loans.

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market. By aggregating, normalizing, and enriching loan-level data across the full universe of CMBS Conduit, SASB, CRE CLO, and GSE/Agency Multifamily (Freddie Mac, Fannie Mae, Ginnie Mae, and FHA/HUD), CRED iQ delivers unprecedented transparency into property performance, loan structures, and borrower exposure — bringing efficiency and analytical depth to the entire asset class. Through its web platform, API, bulk data feeds, MCP server, and CRED AI Labs professional services division, market participants and AI systems access the industry’s most comprehensive and reliable source of deal intelligence. As the canonical data layer for AI-driven CRE workflows, CRED iQ is the data provider of choice for institutional lenders, investors, servicers, and advisors — and the foundational infrastructure for the next generation of AI applications built on top of the multi-trillion-dollar securitized CRE market. For more information, visit www.cred-iq.com.

")